BEPS forms: due date for filing transfer pricing is approaching!

Like many other countries, Belgium has introduced the transfer pricing documentation requirements from the OECD ‘BEPS’ (Base Erosion and Profit Shifting) action plan. In short, multinational groups being present in Belgium through a company or permanent establishment need to assess whether they are required to file a master file, local file and/or country-by-country report with the Belgian tax administration.

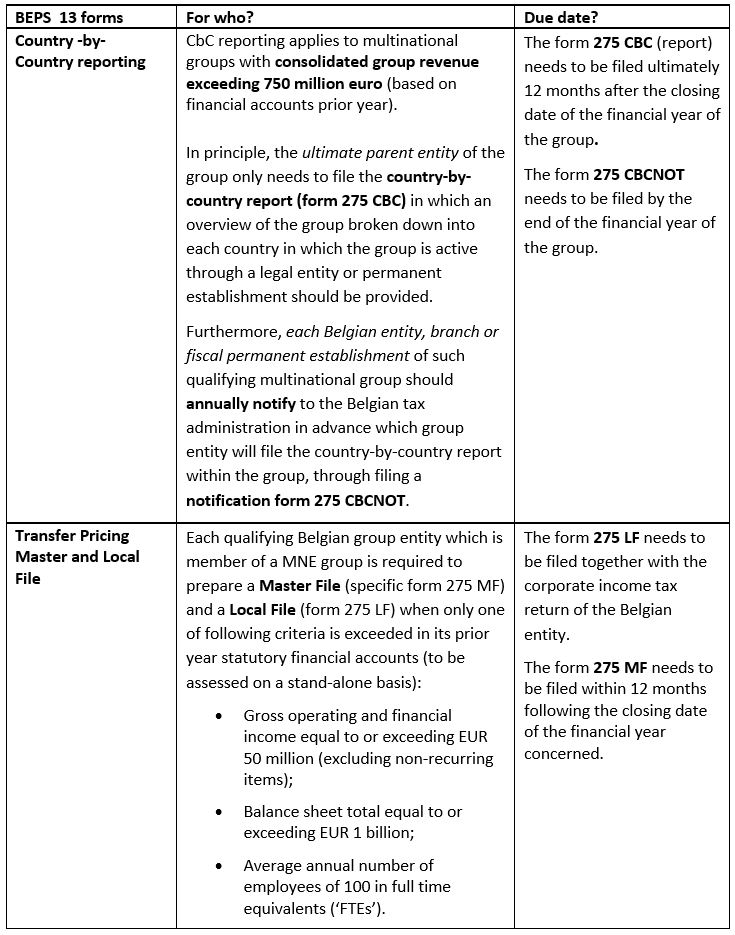

Overview Belgian transfer pricing requirements

We refer to our previous tax alert (see article ‘New transfer pricing forms published as from financial year 2016‘) for more information regarding the Belgian Transfer pricing documentation requirements.

Ultimate due date 31 March 2018

Note that the Belgian Tax Authorities have granted a general extension until 31 March 2018 for the submission of following forms (for which the initial due date was 31 December 2017):

- The Master file (form 275 MF) for tax year 2017 (accounting years starting as from 1st January 2016)

- The Country-by-Country report (form 275 CBC) for tax year 2017

- The Country-by-Country notification (form 275 CBCNOT) for tax year 2018

Submission method

The aforementioned documents should in principle be submitted through the electronic channel ‘My MinfinPro’ in XML format.

An exemption on the latter submission method exists for following forms, which can still be submitted by e-mail towards the competent Belgian tax office:

- The form 275LF and the form 275 CBCNOT related to tax year 2017 (reporting period running until 30th December 2017)

- BEPS 13 forms to be submitted by companies with no Belgian legal representative and/or companies which have been subject of an acquisition, merger or liquidation mentioning that they benefit from the Administrative tolerance granted for such entities.

Note that the preparation and submission process of these transfer pricing forms require some administrative efforts. A timely take-off is therefore highly recommended. Our international tax team can guide you through this administrative process and assist you with meeting the filing requirements.

At Van Havermaet International, we would be pleased to provide you with more in-depth information, to assess your situation and assist you with the preparation and filing of transfer pricing documentation in cooperation with our worldwide network.

Publication date: 13 February 2018